Tax Deducted at Source (TDS) is one of the most critical compliance obligations

for businesses, professionals, and individuals in India. With the new

Income Tax Act, 2025 coming into effect, TDS provisions are now governed

under Section 393 of the new Act — applicable from FY 2026–27 onwards.

This comprehensive rate chart covers all key TDS sections, threshold limits,

and applicable rates — for both residents and non-residents — to help you

stay compliant and avoid penalties.

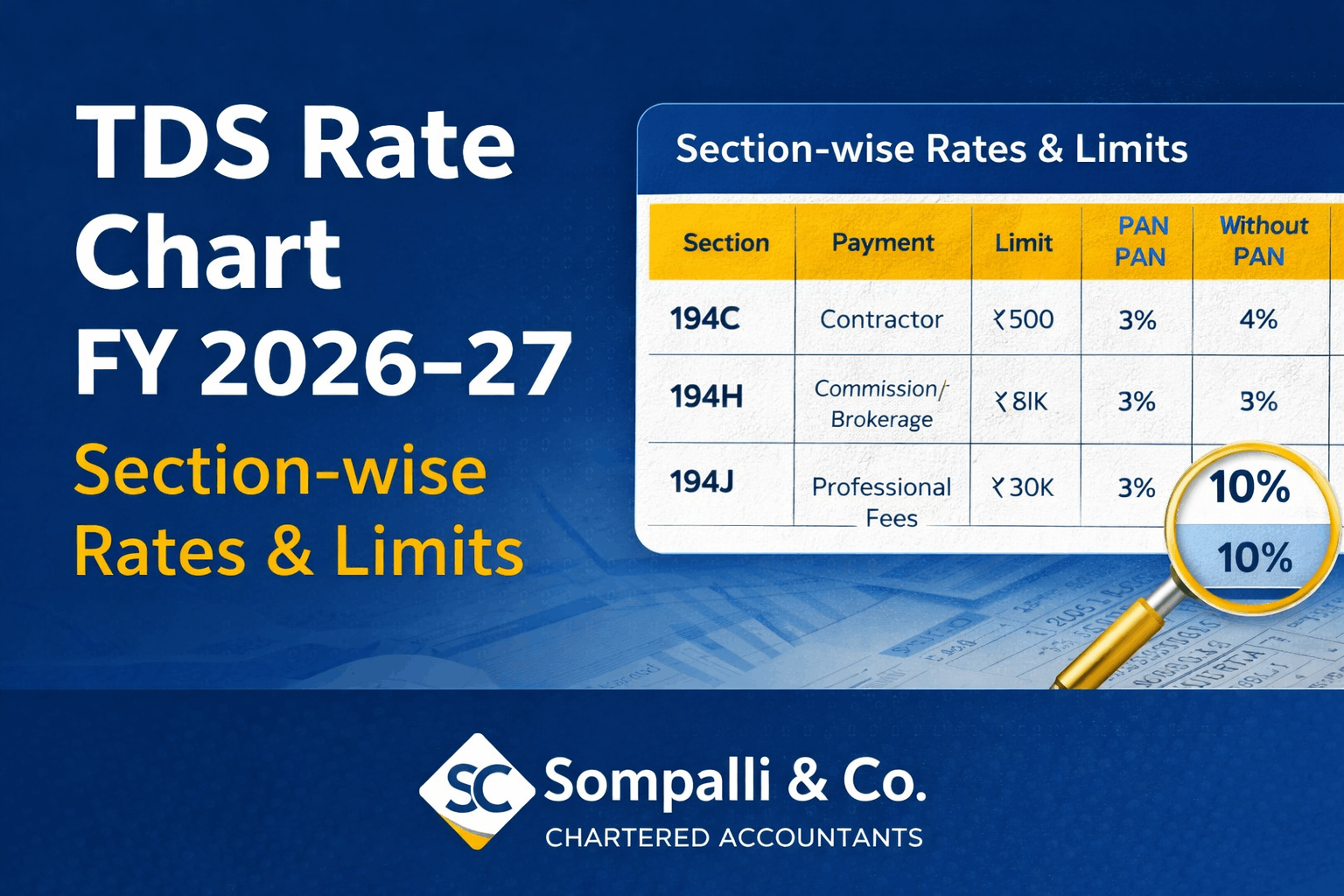

📋 TDS Rate Chart for Residents — FY 2026–27

Note: Section numbers referenced below are as per the Income Tax Act, 1961,

retained for reference purposes.

| Section | Nature of Transaction | Threshold Limit | TDS Rate |

|---|---|---|---|

| 192 | Salary | Basic exemption limit of employee | Slab Rates |

| 192A | Premature withdrawal from EPF | ₹50,000 | 10% |

| 193 | Interest on Securities | ₹10,000 | 10% |

| 194 | Dividends | ₹10,000 | 10% |

| 194A | Interest on bank/post office deposits | ₹50,000 | 10% |

| 194A | Interest on bank/post office deposits (Senior Citizens) | ₹1,00,000 | 10% |

| 194A | Interest – Others | ₹10,000 | 10% |

| 194K | Dividend payment by Mutual Funds | ₹10,000 | 10% |

| 194B | Lottery, game shows, gambling winnings | ₹10,000 | 30% |

| 194BA | Online gaming winnings | No threshold | 30% |

| 194BB | Winnings from horse races (aggregate in FY) | ₹10,000 | 30% |

| 194C | Payment to contractors / sub-contractors | ₹30,000 (single) or ₹1 lakh (FY) | 1% (Individuals/HUF), 2% (Others) |

| 194D | Insurance Commission | ₹20,000 | 2% (Individuals/HUF), 10% (Others) |

| 194DA | Payment from Life Insurance Policy | ₹1 lakh | 2% |

| 194EE | Payment from National Savings Scheme (NSS) | ₹2,500 | 10% |

| 194G | Lottery Commission | ₹20,000 | 2% |

| 194H | Commission / Brokerage | ₹20,000 | 2% |

| 194J(a) | Fees – Technical Services, Call Centre, Royalty, Film Distribution | ₹50,000 | 2% |

| 194J(b) | Fees – All Other Professional Services | ₹50,000 | 10% |

| 194I(a) | Rent – Plant & Machinery | ₹50,000 | 2% |

| 194I(b) | Rent – Land, Building & Furniture | ₹50,000 | 10% |

| 194IA | Transfer of immovable property (other than agricultural land) | ₹50 lakh | 1% |

| 194IB | Rent payment by Individual/HUF not covered u/s 194I | ₹50,000 per month | 2% |

| 194IC | Payment under Joint Development Agreement | No threshold | 10% |

| 194LA | Compensation on transfer of immovable property | ₹5 lakh | 10% |

| 194LBA | Certain income from units of a business trust | No threshold | 10% |

| 194LBB | Income from investment fund units | No threshold | 10% |

| 194LBC | Income from investment in securitisation trust | No threshold | 10% |

| 194M | Contracts, Brokerage or Professional Fees by Individual/HUF | ₹50 lakh | 2% |

| 194N | Cash withdrawal exceeding ₹1 crore (₹3 crore for co-op societies) | ₹1 crore | 2% |

| 194N | Cash withdrawal – ITR not filed for 3 preceding years (₹20L–₹1Cr) | ₹20 lakh | 2% |

| 194N | Cash withdrawal – ITR not filed for 3 preceding years (above ₹1Cr) | ₹1 crore | 5% |

| 194O | TDS on e-commerce participants | ₹5 lakh | 0.10% |

| 194P | Specified Senior Citizens (above 75 yrs) – Salary & Interest | No threshold | Slab Rates |

| 194Q | Purchase of goods exceeding ₹50 lakh | ₹50 lakh | 0.10% |

| 194R | Benefits or perquisites of business/profession | ₹20,000 | 10% |

| 194S | Transfer of Virtual Digital Assets (other than specified persons) | ₹10,000 | 1% |

| 194S | Transfer of Virtual Digital Assets (specified persons) | ₹50,000 | 1% |

| 194T | Payments by Partnership Firms to Partners | ₹20,000 | 10% |

🌐 TDS Rate Chart for Non-Residents — FY 2026–27

| Section | Payment Type | TDS Rate |

|---|---|---|

| 192 | Salary | Normal Slab Rate |

| 192A | Accumulated balance of taxable provident fund | 10% |

| 194B | Winnings from lotteries, card games, gambling, etc. | 30% |

| 194BA | Winnings from online games | 30% |

| 194BB | Winnings from horse races | 30% |

| 194E | Payment to non-resident sportsmen / sports associations | 20% |

| 194EE | Deposits under National Savings Scheme | 10% |

| 194F | Repurchase of units by Mutual Fund or UTI | 20% |

| 194G | Commission on sale of lottery tickets | 2% |

| 194LB | Interest on infrastructure debt fund | 5% |

| 194LBA(2) | Income u/s 10(23FC)(a) | 5% |

| 194LBA(2) | Income u/s 10(23FC)(b) | 10% |

| 194LBA(3) | Income u/s 10(23FCA) from business trust to unit holders | 30% |

| 194LBB | Income from investment fund (other than exempt u/s 10(23FBB)) | 30% |

| 194LBC | Income from securitisation trust (u/s 115TCA) | 30% |

| 194LC | Interest on long-term bond/RDB listed on IFSC | 4% |

| 194LC | Bonds specified above, issued after 01-04-2023 | 9% |

| 194N | Cash withdrawals exceeding ₹1 crore | 2% |

| 194N | Cash withdrawals ₹20L–₹1Cr (ITR not filed – 3 yrs) | 2% |

| 194N | Cash withdrawals above ₹1Cr (ITR not filed – 3 yrs) | 5% |

| 194T | Salary, remuneration, commission, bonus or interest to partners (exceeding ₹20,000) | 10% |

💼 Section 195 — Other Payments to Non-Residents

| Nature of Income | TDS Rate |

|---|---|

| Long-term capital gains u/s 115E (NRI) | 20% |

| Long-term capital gains u/s 112 (sub-clause iii) | 12.50% |

| Long-term capital gains u/s 112A (exceeding ₹1,25,000) | 12.50% |

| Short-term capital gains u/s 111A | 12.50% |

| Any other long-term capital gains | 20% |

| Dividend from IFSC unit | 12.50% |

| Dividend – Others | 10% |

| Interest on foreign-currency borrowings (Govt / Indian concern) | 20% |

| Royalty – specified book copyrights or computer software u/s 115A | 20% |

| Royalty – other (Govt approved agreements) | 20% |

| Fees for technical services (Govt/approved agreements) | 20% |

| Any other income | 20% |

🧾 TCS Rate Chart — FY 2026–27

Note: With effect from 1st April 2026, TCS provisions are governed under

Section 394 of the Income Tax Act, 2025. Section references below are as

per the Income Tax Act, 1961, retained for reference purposes.

| Section | Particulars | Threshold Limit | TCS Rate |

|---|---|---|---|

| 206C(1) | Alcoholic liquor for human consumption | Not applicable | 2% |

| 206C(1) | Tendu leaves | Not applicable | 2% |

| 206C(1) | Timber (forest lease or other mode) | Not applicable | 2% |

| 206C(1) | Scrap | Not applicable | 2% |

| 206C(1) | Minerals (coal, lignite, iron ore) | Not applicable | 2% |

| 206C(1C) | Parking lot, toll plaza, mining & quarrying | Not applicable | 2% |

| 206C(1F) | Sale of motor vehicle | ₹10 lakh | 1% |

| 206C(1G) | Foreign remittance under LRS – education/medical | ₹10 lakh | 2% |

| 206C(1G) | LRS – other purposes | ₹10 lakh | 20% |

| 206C(1G) | Overseas tour programme package | No threshold | 2% |

⚠️ Key Points to Remember

- Higher TDS for non-filers: If a deductee has not filed ITR for the

preceding 3 years, higher TDS rates apply under Section 206AB - DTAA benefit: For non-residents, TDS shall be deducted at the DTAA rate

if it is lower than the applicable TDS rate - Excess TDS refund: Any excess TDS deducted can be claimed as a refund

at the time of filing your Income Tax Return (ITR) - Surcharge & cess: Applicable surcharge and health & education cess must

be added to TDS rates wherever applicable for non-residents

📌 Why Timely TDS Compliance Matters

- Avoids interest under Section 201(1A) for late deduction or deposit

- Prevents disallowance of expenses u/s 40(a)(ia) in business income

- Protects deductors from penalty proceedings under Section 271C

- Ensures smooth TDS return filing (Form 24Q, 26Q, 27Q) within due dates

Final Note

Staying updated on TDS rates and thresholds is essential for every

business owner, finance professional, and individual taxpayer. With the

transition to the Income Tax Act, 2025, it is especially important to

review your TDS compliance framework for FY 2026–27.

At Sompalli & Co., we assist businesses and individuals with end-to-end

TDS compliance — from deduction and deposit to quarterly return filing and

notice responses. Get in touch with us for a compliance review tailored

to your business needs.

Disclaimer: This article is intended for general informational purposes only

and does not constitute professional tax or legal advice. Rates are subject to

change as per government notifications. Please consult a qualified Chartered

Accountant for advice specific to your situation.